Corporate tax cuts have sparked a heated debate in the U.S., particularly in the context of the 2017 Tax Cuts and Jobs Act, which dramatically lowered corporate tax rates from 35% to 21%. This legislation aimed to stimulate economic growth and enhance business investments, yet it has led to a contentious dialogue among policymakers. Recent analyses, notably the Chodorow-Reich analysis published in the Journal of Economic Perspectives, provide insights into the efficacy of these corporate tax cuts, highlighting both the modest wage increases and the significant decline in tax revenue that followed. As Congress approaches a critical juncture in tax reform discussions, voters are increasingly concerned about the implications of these cuts on broader economic stability. The outcomes of these corporate tax policy changes will not only shape the fiscal landscape but also set the tone for future U.S. tax policy and its impact on economic growth.

In recent years, the conversation surrounding financial incentives for businesses has gained unprecedented momentum, especially with the recent framework of business tax reductions. The sweeping changes introduced by the 2017 Tax Cuts and Jobs Act represent one of the most significant shifts in fiscal policy aimed at enhancing corporate profitability. This piece of legislation sought to create a more favorable environment for investment by slashing corporate tax rates and fostering growth opportunities. As lawmakers prepare for the upcoming discussions on tax reform, understanding the effects of these diminutions in corporate taxation becomes crucial. The impact of these strategic financial shifts on business behavior and economic performance continues to be a focal point in debates among economists and policymakers alike.

The Impact of the Tax Cuts and Jobs Act on Corporate Tax Rates

The Tax Cuts and Jobs Act (TCJA) significantly transformed the landscape of corporate taxation in the United States by slashing corporate tax rates from 35% to 21%. This substantial decrease aimed to stimulate business investments and encourage companies to reinvest their profits domestically. However, economic analyses, such as the recent study by Gabriel Chodorow-Reich, reveal that while some investments may have increased, the overall effect on long-term wage growth and corporate tax revenue has been limited. Critics argue that an undue focus on corporate tax cuts fails to address the broader needs of the economy and may undermine essential revenue streams for public programs.

Chodorow-Reich’s analysis indicates that many of the positive outcomes predicted by proponents of the TCJA did not materialize as expected. While a modest uptick in wages and a revitalization of business investments were noted, they did not sufficiently compensate for the considerable drop in corporate tax revenue. This suggests that the initial intention behind the TCJA—to create a self-sustaining cycle of revenue generation through growth—has fallen short of its goals, prompting renewed discussions about revising corporate tax policies.

Evaluating Business Investments Post-TCJA

One of the central aims of the TCJA was to boost business investments through favorable tax treatment, including provisions for immediate expensing of capital investments. Chodorow-Reich’s research highlights that these targeted provisions were indeed more effective in driving investments than blanket corporate rate cuts. The evidence suggests that businesses responded favorably to policies that allowed them to write off costs quickly, thereby enhancing their ability to invest in growth-promoting activities. These findings challenge the notion that lower tax rates alone are the most effective motivator for investment.

Furthermore, while the TCJA did catalyze some investment increases—reported at around 11%—the actual economic impact on job creation and wage growth was less robust than anticipated. This indicates a complex interplay between tax policy and economic outcomes. As lawmakers contemplate the future of corporate taxation, it may be prudent to focus on reinstating targeted incentives for investments rather than relying solely on rate cuts as a means of stimulating the economy.

Rethinking Corporate Tax Cuts in an Election Year

As the 2025 elections approach, the debate over corporate tax cuts is likely to intensify. Political leaders from both parties are sharpening their rhetoric to capture voter attention on economic matters, particularly those pertaining to the expiration of parts of the TCJA. Democrats, for instance, are advocating for higher corporate tax rates to fund social programs, while Republicans argue that further cuts will promote growth and competition. Amidst this political clash, it is essential to sift through the data—like that presented by Chodorow-Reich—to discern the actual impacts of these policies.

The electoral discourse surrounding corporate tax rates often neglects nuanced economic studies, which indicate that merely lowering tax rates does not guarantee a corresponding increase in investments or job growth. As such, voters and policymakers alike should consider a balanced approach that not only evaluates the effectiveness of tax cuts but also explores alternative measures that could achieve desired economic outcomes, ensuring a comprehensive understanding of how taxation influences corporate behavior.

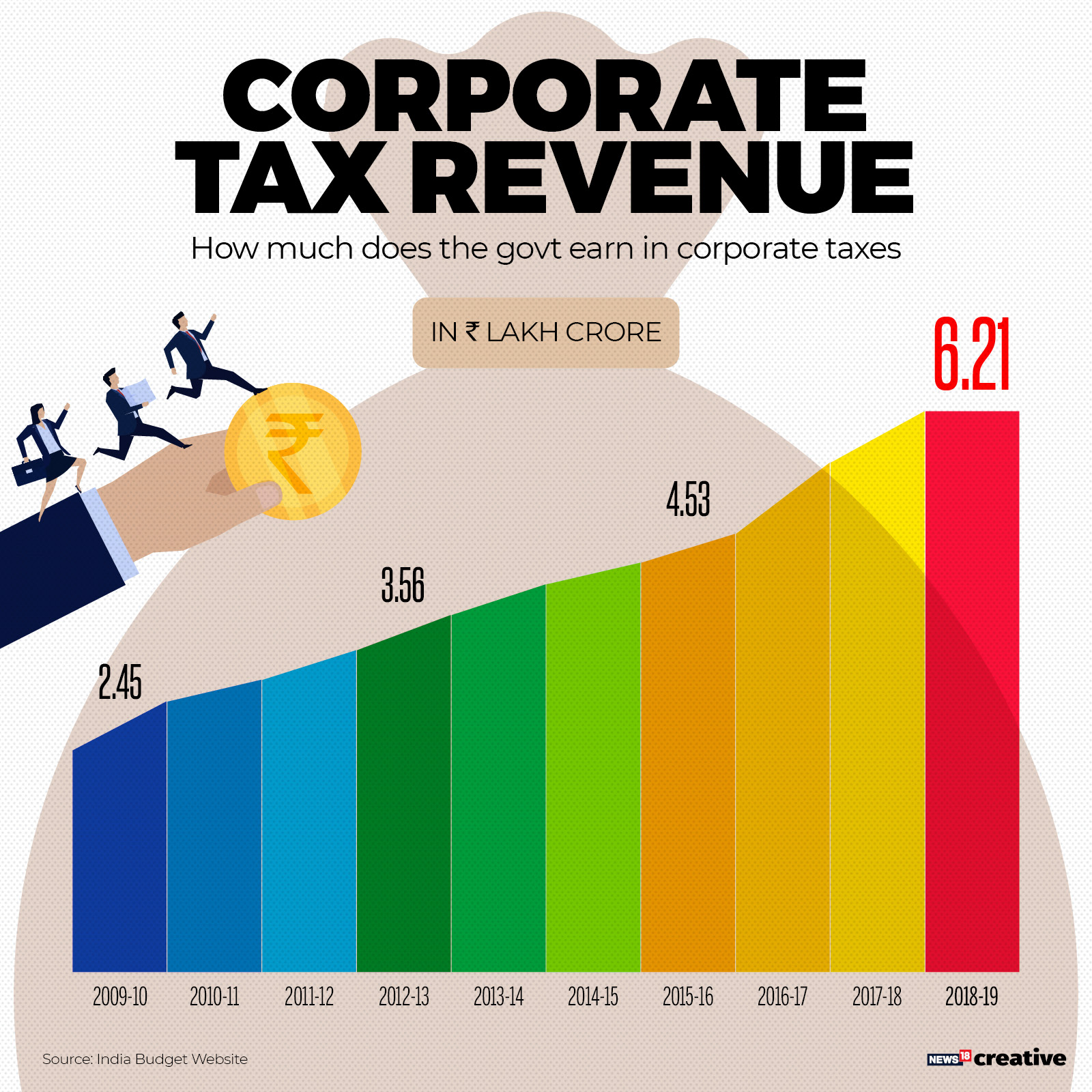

Analyzing Corporate Tax Revenue Fluctuations

Another critical aspect of the TCJA’s legacy is the fluctuation in corporate tax revenue it generated. Initially, the corporate tax revenue experienced a sharp decline of approximately 40% following the implementation of the law. However, by 2020, there were surprising rebounds in revenue as businesses benefitted from the tax cuts and responded to the unprecedented economic context shaped by the pandemic. Such developments illustrate the complex dynamics between tax policy and broader economic factors, including corporate profits during times of crisis.

Chodorow-Reich’s findings indicate that while corporate profits soared, the reasons behind this phenomenon require further examination. Factors such as shifts in global tax practices and adjustments in corporate strategies played roles in this revenue resurgence. As policymakers look ahead, maintaining a flexible approach to corporate tax policy might be crucial in adapting to evolving economic landscapes and ensuring sustainable revenue generation.

Exploring the Relationship Between Tax Policy and Wage Growth

The TCJA was expected to drive significant wage growth for employees, with initial forecasts estimating increases of up to $9,000 per full-time worker. However, Chodorow-Reich’s research provides a more conservative assessment, suggesting an actual wage increase closer to $750 per year. This disparity highlights the critical need to critically evaluate the assumptions underlying tax cut proposals, particularly those promising widespread economic benefits stemming from corporate tax reductions.

Understanding the relationship between corporate taxation and wage growth requires a nuanced exploration of economic data and expectations. It appears that while corporate tax cuts can potentially facilitate business expansion, they do not automatically translate into substantial wage increases for workers. As we reflect on the implications of the TCJA, it becomes evident that a multifaceted approach to taxation and economic policy is vital for fostering genuine wage growth and improving living standards for the broader workforce.

Future Directions for US Tax Policy

Looking forward, US tax policy will undoubtedly face rigorous scrutiny as the expiration of key provisions of the TCJA looms in 2025. Legislators will need to grapple with balancing the needs for revenue generation against the political pressures to maintain or enhance corporate tax cuts. Given the mixed results produced by the TCJA, discussions about reforming the taxation framework may shift from merely cutting rates to considering a comprehensive strategy that addresses various economic challenges.

One potential avenue for reform could involve a dual approach that includes increasing corporate tax rates while simultaneously reinstating effective investment incentives. By facilitating targeted tax benefits for capital expenditures, lawmakers could encourage growth while maintaining a balanced revenue stream for essential public services. Such an approach would signify a shift towards more evidence-based policy decisions, breaking away from enduring partisan divides in favor of collaborative solutions that drive sustainable economic growth.

The Role of Economic Studies in Tax Policy Decisions

The ongoing debate over corporate tax cuts underscores the importance of grounding tax policy discussions in empirical research and economic studies. Chodorow-Reich’s rigorous analysis of the TCJA provides valuable insights that challenge conventional wisdom surrounding tax cuts. By revealing underwhelming outcomes regarding wage growth and revenue volatility, such research serves as a critical reminder of the need for informed decision-making in crafting effective tax legislation.

As political narratives often dominate public discourse, incorporating data-driven insights into discussions about corporate taxation can lead to more robust and equitable outcomes. Engaging with economic studies allows policymakers to understand the real implications of tax decisions, ensuring that future legislation fosters a healthier economic environment. Therefore, promoting a culture of evidence-based policymaking will be essential for adapting to the changing economic midlands at both corporate and individual levels.

Corporate Tax Policy and Global Competitiveness

In an increasingly globalized economy, the competitive position of the United States hinges significantly on its corporate tax policy. As many countries have slashed corporate tax rates to attract business investments, the U.S. faced pressure to follow suit—culminating in the sweeping changes brought by the TCJA in 2017. This competitive landscape requires ongoing evaluations of how tax rates impact corporate behaviors and the attractiveness of the U.S. market compared to other nations.

Moreover, as seen in Chodorow-Reich’s analysis, effective taxation must balance competitiveness with the need for adequate public funding. While lower corporate tax rates may incentivize business operations and repatriation of profits, they could simultaneously suppress vital government revenues. Policymakers will need to find the right equilibrium to ensure that corporate tax policy not only promotes business innovation but also sustains the funding necessary for infrastructure, education, and other public services.

Political Divide Over Corporate Tax Cuts: A Closer Look

The political divide regarding corporate tax cuts is not merely a matter of ideology; it is also a reflection of divergent priorities for economic growth and social welfare. Proponents of tax cuts argue that lower corporate taxes are essential for stimulating business growth and increasing job creation, amplifying the voices of traditional economic theories that advocate for supply-side economics. On the flip side, opponents assert that tax cuts disproportionately benefit wealthier corporations, detracting from public investment needs and exacerbating income inequality.

Chodorow-Reich’s research adds a critical layer of complexity to this debate, emphasizing that the anticipated benefits of corporate tax cuts are not always realized in practice. With so much at stake in an election year, it is imperative for voters to engage with these debates and understand the nuanced implications of each party’s stance on corporate tax policy. This will foster a more informed electorate able to advocate for policies that align with their economic interests and promote holistic well-being.

Frequently Asked Questions

What are corporate tax cuts and how do they impact the economy?

Corporate tax cuts refer to reductions in the tax rate that corporations must pay on their profits. Such cuts, like those introduced by the Tax Cuts and Jobs Act (TCJA) of 2017, are debated for their potential to stimulate economic growth through increased business investments and job creation. However, evidence from studies suggests that while investments may increase modestly, the overall impact on wages and tax revenue can be limited.

How did the Tax Cuts and Jobs Act affect corporate tax rates in the US?

The Tax Cuts and Jobs Act significantly reduced the corporate tax rate from 35% to 21%, marking one of the largest cuts in US history. This change aimed to make the US more competitive globally and to encourage business investments. However, analyses indicate that the resulting increase in corporate profits did not fully offset the foregone tax revenue.

What is the Chodorow-Reich analysis regarding corporate tax cuts?

The Chodorow-Reich analysis, published by economist Gabriel Chodorow-Reich and colleagues, evaluates the impacts of the Tax Cuts and Jobs Act on corporate tax cuts. It highlights that while there was a reported increase in business investments by about 11%, these gains were not sufficient to counteract the substantial decline in corporate tax revenue, which fell by 40% initially following the implementation of the TCJA.

What are the effects of corporate tax cuts on business investments?

Corporate tax cuts such as those from the Tax Cuts and Jobs Act are intended to incentivize business investments by allowing firms to retain more profits. Research indicates that while there was a modest increase in capital investments post-TCJA, many experts argue that targeted expensing provisions provided more effective incentives for growth than broad tax rate reductions.

In the context of US tax policy, what are the implications of expiring corporate tax cuts?

As certain provisions of the Tax Cuts and Jobs Act expire, there may be significant implications for US tax policy, including potential increases in corporate tax rates. This could lead to renewed debates on how to balance budgetary needs with fostering an environment conducive to business growth and investment.

How do corporate tax cuts relate to wage growth?

Supporters of corporate tax cuts argue that reducing tax burdens on companies leads to higher wages for workers, as firms invest in new capital and expand their operations. However, evidence from the Chodorow-Reich analysis suggests that the actual wage increase associated with the TCJA was lower than anticipated, indicating that tax policy alone may not be sufficient to drive substantial wage growth.

Why are corporate tax cuts a controversial topic in US politics?

Corporate tax cuts, especially those enacted by the Tax Cuts and Jobs Act, are controversial due to divergent viewpoints among lawmakers. Proponents argue that they promote economic growth and job creation, while opponents highlight concerns about reduced tax revenues and inequality. The debate often intensifies around election periods, as these cuts can be used as political tools to sway voter opinion.

What lessons can be learned from the analysis of corporate tax cuts in the TCJA?

The analysis of corporate tax cuts under the TCJA reveals that while reducing corporate tax rates can incentivize certain investments, the overall benefits may not be as pronounced as initially hoped. Policymakers should consider a comprehensive approach, including targeted tax incentives and provisions that directly benefit both businesses and workers, rather than relying solely on rate cuts.

| Key Point | Details |

|---|---|

| Corporate Tax Cuts | The TCJA significantly reduced the corporate tax rate from 35% to 21%, aiming to stimulate the economy. |

| Impact on Revenue | The corporate tax revenue initially decreased by 40% after the TCJA was implemented, but revenues surged beyond expectations from 2020 onward. |

| Wage Increase Predictions | Initial predictions estimated wage increases of up to $9,000, but later studies suggested a more realistic increase of about $750 annually. |

| Investment Effects | Capital investments increased by approximately 11% post-TCJA, showing some responsiveness to corporate tax policy. |

| Future Tax Discussions | As key provisions are set to expire in 2025, debate continues over whether to raise corporate tax rates or maintain tax cuts. |

| Partisan Perspectives | Democrats advocate for raising corporate tax rates to fund programs, while Republicans promote further cuts for growth. |

Summary

Corporate tax cuts are a pivotal topic in today’s economic discussion, especially as lawmakers prepare for debates leading into 2025. The 2017 Tax Cuts and Jobs Act, which lowered the corporate tax rate significantly, ignited a partisan dialogue about the implications of such cuts. Economists continue to analyze the effectiveness of these cuts on corporate investments and revenues, revealing nuanced effects on both growth and government funding. As the expiration of key provisions approaches, the need for a balanced approach to corporate taxation becomes increasingly crucial.